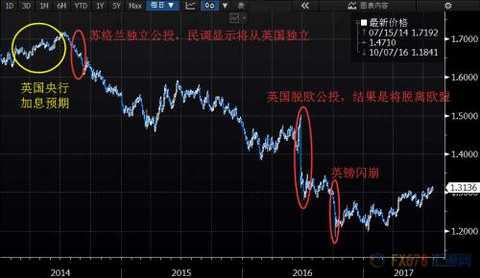

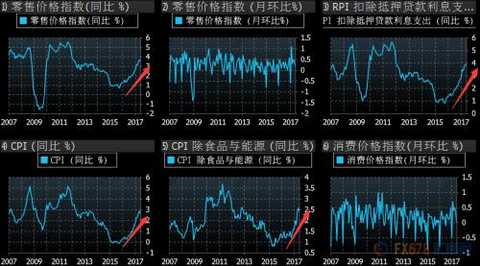

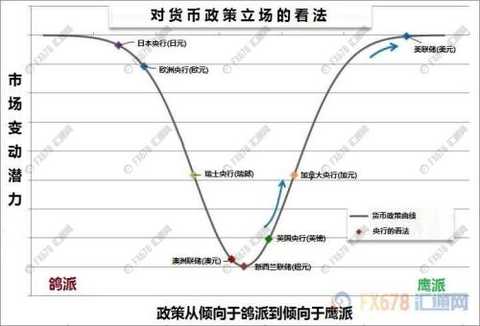

The Fed maintained interest rates as expected in July and said it would soon begin to implement the balance sheet normalization plan. This means that as long as there are not too many accidents, the Fed began to shrink in September or has been "iron nailed." The Fed’s monetary policy is well known, and will the other seven central banks follow suit? ★ By the middle of the year, the Fed has almost finished the year-round policy. On the morning of July 27th (Thursday), Beijing time, the Federal Reserve announced the July interest rate decision and decided to keep the federal funds rate unchanged at 1.00-1.25%, almost in line with market consensus. At the same time, in the published policy statement, the Fed hinted to the market with the word “very fast†that as long as the economic data for the next 8 weeks is roughly in line with expectations, or if there is not much deviation, then the Fed will be at 9 The plan for the reduction of the balance sheet was announced at the monthly meeting. Huitong.com Xiaobian once said in the article in early July that the Fed’s urgency to raise interest rates is actually not as “shrinkingâ€. Judging from the July policy statement, is the variable still certain? The second policy path conjecture put forward in the article of the Federal Reserve's Monetary Policy Conjecture in the Second Half of 2017 is a more practical idea. The Fed opened the “reduction table†in September and then completed another interest rate hike in December. (Huitong.com reminded that the Fed will announce the interest rate decision next time at 02:00 on September 21st, Beijing time. It will also announce the latest economic forecast and "lattice map". Later, at 02:30, Chairman Yellen will also hold a news. Conference.) The Fed said, "If the economic development is basically in line with expectations, the balance sheet normalization plan will soon be implemented." It is this "very fast" word that is considered by the market to be the next (September) meeting. In describing inflation, the Fed said that “the overall year-on-year growth rate of core inflation and core inflation, which excludes energy and food prices, has fallen, with inflation levels below 2%.†Compared with the previous policy statement, the Fed deleted the qualifier "recent", at least indicating that the Fed's concerns about the inflation slowdown may not be temporary. At the same time, it has been confirmed by changing the “inflation level has been slightly below 2%†to “inflation level below 2%â€. This change in attitude is enough to prompt the Fed to be cautious about raising interest rates in September and even November meetings (no press conference). According to the probability of the federal funds rate futures, as of July 28, traders believe that the Fed’s probability of raising interest rates in December this year is 46.7%, slightly lower than 50%, which is enough to show that the current market will add another interest to the Fed during the year. The outlook is not optimistic. (Figure 1: As of July 28, 2017, the Fed’s probability-of-interest probability distribution map, the market is cautious about the prospect of the Federal Reserve’s interest rate increase during the year) Of course, in addition to employment and inflation, the Fed said it will also pay attention to “indicating the financial market and the development of international situationâ€. This may be related to the turmoil of President Trump's entry into the White House for half a year, including the resignation of officials, the investigation of the Russian-Russian door, the repeated failure of the medical reform bill, and the promise of campaigning to increase infrastructure spending and tax reform. However, the Fed will eventually make decisions based on economic data and data expectations, so before they see that political uncertainty has a tangible effect on the economy, they will probably not pay much attention to the government. ★ Be wary of the Bank of Canada to accelerate the risk of raising interest rates For the US neighbor, Canada, it is the first country in the G10 to follow the Fed rate hike. On July 28th (Friday), Canada's May GDP data was released. The results showed that it exceeded expectations. The annual growth rate recorded 4.6%, much higher than the expected 4.1% and the previous value of 3.3%. Since the oil price collapse in the summer of 2014, Canada has begun to seek economic transformation, trying to get rid of heavy dependence on oil prices. At the moment, it seems that the transformation has been effective. At a press conference after the interest rate decision in July, Bank of Canada Governor Poloz showed an optimistic view of the Canadian economy. He said that Canada's economic situation no longer needs to be supported by monetary stimulus, and it has seen an increase in wage inflation. Judging from the probability of interest rate hike implied by overnight swap rates, the market believes that the time point for the Bank of Canada's next rate hike is likely to be at the end of October, with a probability of 75.2%, and just two months ago, the market for Canadian interest rates is at 1 The probability of % is almost 0%. Currently, the Canadian interest rate is 0.75%. (Figure 2: As of July 28, 2017, the Bank of Canada raises interest rate distribution map, the market believes that the central bank will raise interest rates next time in October) (Figure 3: As of July 28, 2017, the Bank of Canada's October interest rate level probability distribution comparison chart, 2 months ago, the market believes that the probability of Canada's interest rate at 1% is almost 0) If the Canadian economy can continue to accelerate recovery, then the central bank's accelerated tightening of monetary policy may also be a matter of course. For the market, as long as you follow the country's economic data, you may be able to find clues about the Bank of Canada's future policy. ★ Bank of England, the next central bank most likely to raise interest rates Given that the Fed and the Bank of Canada have already increased interest rates, the next one is likely to raise interest rates most likely to be the Bank of England. Beijing time on August 3 (Thursday) at 19:00 is the best time to observe the attitude of the Bank of England. At that time, the Bank of England will announce the quarterly inflation report in addition to the August interest rate resolution and meeting minutes. After 19:30, Bank of England Governor Carney will join hands with Vice President Broadbent to attend the press conference to fully communicate with the market. Since the 2016 Brexit referendum, it has been more than a year since the blink of an eye. The pound against the US dollar also plunged from the then high of 1.5018 all the way, refreshing the low level of 1.1841 over the past 30 years. In fact, the bear market in the pound against the US dollar can be traced back to July 2014 three years ago. In the first half of 2014, the market once expected the Bank of England to raise interest rates, which was earlier than the Fed’s rate hike expectations. However, due to the polls at the time, the Scottish independence referendum may be independent from the UK, making the pound "all the way south" against the dollar, and the British Brexit vote also hit the pound. (Figure 4: Daily chart of GBP/USD against the US dollar from January 1, 2014 to July 28, 2017) The most direct impact of the plunge in the pound is the rise in inflation/inflation expectations. According to data released by the National Bureau of Statistics of the United Kingdom, consumer prices (CPI) rose by 2.6% in June from the same period last year, exceeding the central bank's 2% target. (Figure 5: UK inflation level observation chart) The Bank of England is surprised by the rate of inflation this year. The bank's latest forecast inflation rate will reach a peak of 2.8% later in 2017, and most analysts expect the inflation rate to rise to at least 3%. The central bank has so far chosen not to raise interest rates to cope with inflation, saying that the British referendum's strike against the pound should be temporary. But some central bank officials have recently hinted that the Bank of England may be about to raise interest rates. Three of the eight monetary policy members voted in favor of raising interest rates in June, but one of them has since retired. Right now, the latest quarterly inflation report to be released in August may provide the basis for the Bank of England's next move. Therefore, it needs to be taken seriously. Judging from the current market expectations, the time window for the Bank of England to raise interest rates next time may be in the middle of next year. However, it is impossible to rule out that two members may vote again in favor of raising interest rates at the August meeting. (Figure 6: As of July 28, 2017, the Bank of England raises interest rate distribution map, the rate hike window may be May 2018) ★ New Zealand Federal Reserve’s monetary policy may face an inflection point Compared with the previous central banks that are raising interest rates or are about to raise interest rates, the attitude of the New Zealand Federal Reserve is neutral. On the one hand, the Fed said that lower exchange rate levels will help balance the country's economic growth, and the devaluation of the New Zealand dollar is necessary to further reduce debt pressure. On the other hand, rising inflation has made the RBNZ no need to cut interest rates further. From the market expectation, the time frame for the New Zealand Federal Reserve to raise interest rates next time is the same as that of the Bank of England, and it will be in the middle of next year. (Figure 7: As of July 28, 2017, the New Zealand Federal Reserve rate hike probability map) However, Huitong.com Xiaobian wants to remind everyone that New Zealand will hold a general election in September, and the current chairman, Wheeler, will also retire on September 27th. The new government officially appoints a new chairman may wait until March next year, so if you consider it from the perspective of uncertainty, then there is reason to believe that the New Zealand Federal Reserve will continue to stand for a long time. ***More reports, please see Huitong.com previously reported that the Fed will be reformed after the New Zealand election. But it has nothing to do with the current chairman Wheeler *** ★ Reserve Bank of Australia or the lower limit of the closed interest rate The Reserve Bank of Australia may be the next central bank to face the policy inflection point of the New Zealand Federal Reserve, but the Reserve Bank of Australia may choose to wait for a while before turning to a rate hike. The last time the Reserve Bank of Australia cut interest rates was almost a year ago, and interest rates have remained at a record low of 1.25% since then. Right now, on August 1 (Tuesday), the Reserve Bank of Australia will announce the latest interest rate resolution. At the same time, the latest quarterly monetary policy report will be released on Friday (August 4th). This is a good time for the market to understand the Fed’s monetary policy. Whether it is the Reserve Bank of Australia's interest rate decision in July, or the Fed Chairman Rowell in his speech on the labor market and monetary policy in July, he has fully affirmed Australia's economic growth and showed optimistic views. But this does not mean that they are about to raise interest rates, because the Reserve Bank of Australia has repeatedly said that the exchange rate appreciation will make the Australian economic adjustment complicated. The slowest salary growth in decades is also a factor they worry about. However, they may not cut interest rates further to stimulate economic growth. Although interest rate cuts can further stimulate inflation and stabilize economic growth, they may cause other troubles, such as adding a fire to the already high housing prices, which may eventually lead to financial stability risks. For the Reserve Bank of Australia, one of the more economical practices is to wait for other central banks to raise interest rates. From another point of view, as long as the Reserve Bank of Australia does not move, it can also open the effect of spreads with other countries. This is similar to the effect of the interest rate cut by the Reserve Bank of Australia in some way. For the Reserve Bank of Australia, why not? From the market expectation, it seems to reflect this. At present, the market believes that the first rate hike by the Reserve Bank of Australia needs to wait at least until the second half of 2018. (Figure 8: As of July 28, 2017, the probability of the rate hike by the Reserve Bank of Australia, the market believes that the Fed’s earliest rate hike also needs to wait until the second half of 2018) ★The Governor of the Swiss National Bank and the two sides rely on the "mouth gun" to suppress the Swiss franc If the interest rates of the central bank in the previous article are all positive, then the three central banks to be mentioned next are the central banks that implement negative interest rates. The Swiss National Bank is one of the five central banks with negative interest rates. The other four are the Swedish central bank, the Danish central bank, the European Central Bank and the Bank of Japan. On July 25th, SNB Governor Jordan once again reiterated that the Swiss franc was overvalued, which caused the Swiss franc to suffer. And Jordan also said that they will not only maintain negative interest rates, but also have room for the operation of the balance sheet. Undoubtedly, his position is relatively dovish. And in the short term, there is no possibility that the central bank will raise interest rates. ***More reports, please see Huitong.com previously reported that "Europe / Rui or the biggest monthly increase in 6 years, and may rise further"*** ★ The European Central Bank will end the ultra-loose policy, but it is still far from the austerity policy. At the end of June, the European Central Bank hinted that it might start tightening monetary policy. According to informed sources, the ECB’s senior management believes that October will be the most likely time to determine the fate of the asset purchase program. People familiar with the matter also said that another possible option from the central bank for December was considered too late. At the end of July, European Central Bank Management Committee Novotny said that he agreed with the opinion of the German central bank governor Weidman that it is time to slowly weaken the stimulus. At the same time, he acknowledged that the European Central Bank has indeed begun to discuss tightening policies. Although it is still necessary to maintain negative interest rates for some time, the problem of distortion is very dangerous. Nowotny also said that it is reasonable to reduce the size of QE from January 2018. European Central Bank Executive Committee member Morsch also expressed a similar point. He said in a speech in Singapore that forward-looking guidance, asset purchases, negative nominal interest rates, and loan programs designed to stimulate bank lending, such as long-term orientation The financing operations (TLTRO) are used to counter the challenges of the time, but as the situation normalizes, these policies are unlikely to remain necessary. As the global economy and central bank policies return to normalization, non-traditional monetary policy instruments taken since the financial crisis may no longer be necessary. However, Morsch’s speech fully echoes the statement made by President Draghi in the policy statement after the July interest rate decision. Morsch emphasized that the continued expansion of the Eurozone economy has brought greater confidence to the European Central Bank, but to raise inflation, it still needs to implement a loose monetary policy to a large extent. However, the European Central Bank Management Committee Lauten Schlegel has issued a different view. She said that there is no trend to rebound towards the inflation target. The low interest rate environment is undoubtedly a challenge in the long run. It is important to be ready to withdraw from the easing policy at the right time. The key is that inflation will have a solid upward trend to reach a target of less than 2%. She believes that it is not yet time to withdraw from the easing. For the European Central Bank, the first thing they should do before they raise interest rates is to reduce the size of quantitative easing (QE), just as the Fed did after 2014. And ending the negative interest rate by the European Central Bank may be even more distant. In any case, the ECB’s monetary policy will be very loose for a long time to come. ★ The Bank of Japan may be the last central bank to enter monetary policy normalization Among the G10 countries, the Bank of Japan is considered to be the last country to normalize monetary policy. At least from the market, the probability of raising interest rates on the central bank can be described as far-reaching. The Bank of Japan is committed to achieving a 2% inflation target, but the central bank’s economic forecast released in July once again delayed the time to achieve inflation targets, the sixth since the launch of the large-scale asset purchase program by Mr. Kuroda in 2013. Delayed. Perhaps hinting that in order to achieve policy goals, they will not stop the super-loose monetary policy. At the end of July, with the post of the former monetary policy committee of the two strong hawks of the Bank of Japan, Sato Kenyu and Takeuchi Hideyoshi, the newly appointed two members vowed to reach a 2% inflation target and said they would discuss withdrawing from large-scale currency. It is still too early to stimulate. Kataoka said that he hopes to see a rapid price target, but he is not sure when it will be reached. Another new member of the Suzuki Division said at a joint press conference that it is dangerous for the market to withdraw from the stimulus policy. This means that the Bank of Japan’s attitude toward monetary policy is unlikely to be more hawkish than before. Although members discussed the information disclosure on the exit easing strategy in the minutes of the June central bank meeting, for a long period of time, it should not be possible to see the day when the Bank of Japan ended its easing policy. ★ Monetary policy normalization position: the Fed takes the lead, the Bank of Japan In summary , if the monetary policy tendencies of the above-mentioned central banks are drawn into a graph, it may be as shown in the following figure: 1 The Fed is leading the process of raising interest rates, but it seems that as the rate hike cycle deepens, the space above will become narrower; 2 The Bank of Canada and the Bank of England should follow the next round of interest rate hikes; 3 For the New Zealand Federal Reserve and the Reserve Bank of Australia, they are now at the threshold of choice and they seem more willing to wait and see; 4 And the dovish of the Swiss National Bank wants to become more dovish or join the neutral policy team with operational space; 5 No matter how the signal is transmitted to the market, it will be interpreted as the hawkish party as the European Central Bank. As for the Bank of Japan, the normalization of monetary policy is far from possible; perhaps because the market has long seen them, there is almost no policy option. Let's go. (Figure 9: Monetary Policy Position Chart) Finally, Huitong.com wants to reiterate the previous view: in the second half of 2017, it may be necessary to revisit the sights back to the world's major central banks, especially the European Central Bank and the Bank of England. Therefore, the annual meeting of the global central bank scheduled to be held in Jackson Hole, USA on August 24-26 is definitely not to be missed. As of press time, ECB President Draghi has made it clear that he will attend the annual meeting, and the market believes that he may release heavy expectations at the meeting. The viewpoint in this article is the personal thinking and understanding of Huitong editors with the wind, and does not make trade references. If you are biased, please bear with me. If you need to reprint, please indicate the source, thank you! Ladies Slipper Socks With Grips Ladies Slipper Socks with grips for Women is great winter socks to warm the cold weather.The elastic bands at the ankle of warm socks for women do not compress your legs, then giving you comfortable wear experience for everyday activities and sleeping with our Cozy Socks for women.The silicone gripper on the bottom of the cozy socks can reduce slippage on smooth floors and Slipper Socks for women grippers can ensure a secure no-slip fit in your slippers, shoes, or sneakers with a cozy feel. Ladies Slipper Socks With Grips,Ladies Bed Socks With Grips,Slipper Socks Womens With Grips,Womens Fuzzy Socks With Grippers jiangyin haorun knitting co.,ltd , https://www.jyhrknitting.com